Firstly, in today’s rapidly evolving financial landscape, agency banking advantages for customers experience has become a crucial differentiator for banks and financial institutions. As customers demand more convenience, personalization, and accessibility, traditional banking methods are giving way to innovative solutions such as white-label agency banking.

What is White-Label Agency Banking Advantages for Customers?

However, white-label agency banking involves the collaboration between a traditional financial institution and a non-banking entity to offer banking services under the brand of the non-banking partner. Essentially, it allows non-banking organizations, like retail stores or fintech companies.

Personalization and Accessibility: Agency Banking Advantages for Customers

Furthermore, One of the primary reasons why white-label agency banking enhances customer experience is the increased personalization it offers. Traditional banking can often feel impersonal, with a focus on standard procedures and limited flexibility.

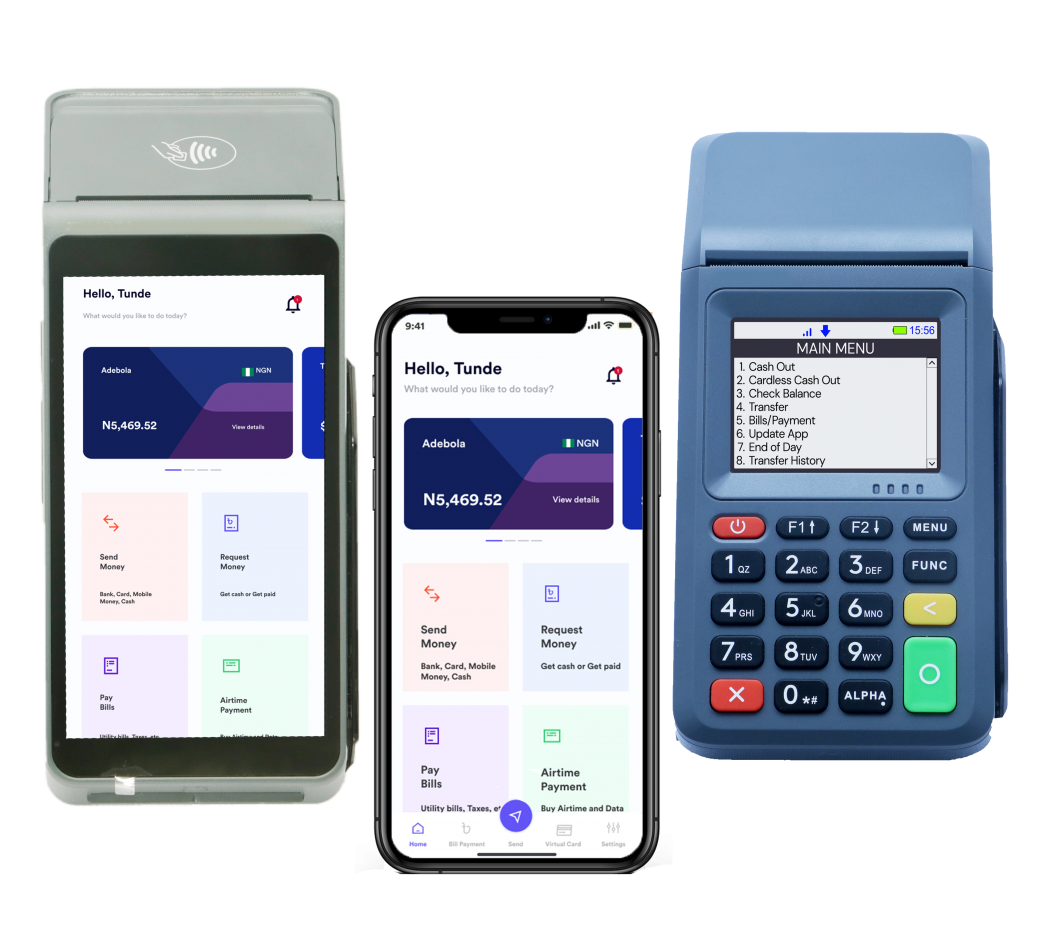

Seamless Integration and Brand Consistency

Moreover, with white-label agency banking, customers experience a seamless integration of banking services into the ecosystem they are already familiar with. The services are integrated into the partner’s platform or app, ensuring a consistent and familiar user interface.

Increased Financial Inclusion

Additionally, white-label agency banking plays a significant role in promoting financial inclusion, especially in areas where traditional banking infrastructure might be limited. By utilizing the existing network of non-banking partners, banks can reach underserved or remote communities.

Enhanced Customer Support and Service

Lastly, collaborating with non-banking partners also opens up new avenues for providing exceptional customer support. These partners are often already well-versed in providing excellent customer service in their respective domains. Banks can extend the same level of customer support.

Conclusion

In conclusion, white-label agency banking is a game-changer in the banking industry, providing a win-win solution for both banks and customers. With its focus on personalization, accessibility, and brand consistency, this innovative approach enhances customer experience and sets a new standard for banking services. Lastly financial institutions can create a lasting impact.