White-label agency banking is making waves in Nigeria’s financial sector, redefining how banks and financial institutions operate. Hence, this blog post explores the impact and opportunities of white-label agency banking in Nigeria. Discover how this innovative solution is transforming the banking landscape, empowering financial institutions to offer personalized services.

The Rise of White Label Agency Banking

With the rapid expansion of Nigeria’s financial market, banks are seeking new avenues to reach a broader customer base. White-label agency banking presents a game-changing solution, allowing banks to collaborate with third-party providers and extend their services beyond traditional branches. This strategic partnership opens doors to previously unexplored territories and fosters financial inclusion for the unbanked and underbanked population.

Benefits of White Label Agency Banking

- Enhanced Customer Reach: White-label agency banking allows banks to establish a network of retail agents in remote or underserved areas. These agents act as intermediaries, offering banking services to customers who may not have easy access to traditional bank branches.

- Tailored Banking Services: Through white-label solutions, banks can tailor their services to cater to the unique needs of the Nigerian market. However, this includes offering services in local languages and incorporating culturally relevant financial products.

- Cost-Effective Expansion: However, setting up physical branches in every region can be costly and time-consuming. White-label agency banking provides a cost-effective way for banks to expand their presence and serve a more extensive customer base.

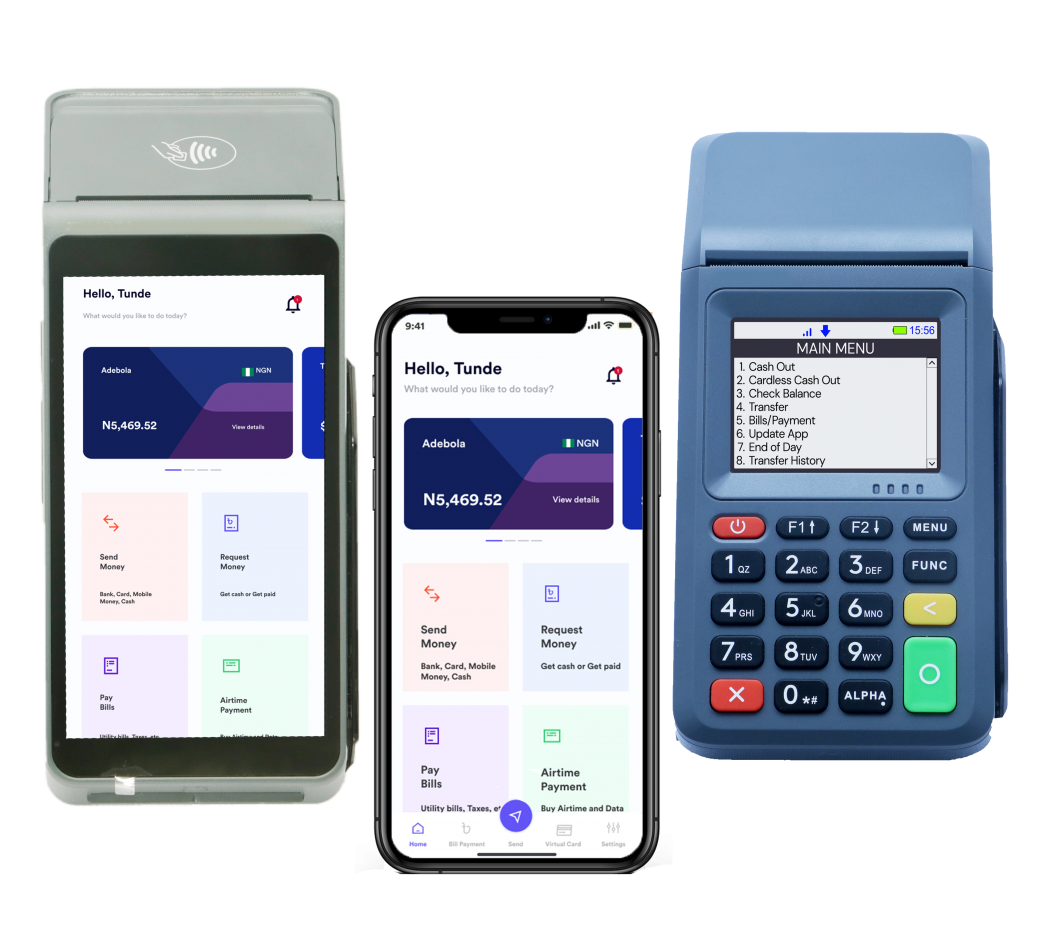

- Technological Advancements: White-label solutions come with advanced technology and digital platforms, enabling seamless and secure transactions. Hence, customers can enjoy modern banking conveniences even in remote areas.

Regulatory Landscape and Compliance

The Central Bank of Nigeria (CBN) regulates the financial sector, including agency banking. Banks must adhere to CBN guidelines and obtain necessary licenses to operate white-label agency banking services. Compliance with regulations ensures customer protection and data security, fostering trust in the banking system.

Challenges and Mitigation Strategies

While white-label agency banking presents exciting opportunities, certain challenges must be addressed:

- Agent Training and Management: Proper training and monitoring of retail agents are essential to ensure quality service delivery and customer satisfaction.

- Security and Fraud Prevention: Robust security measures, such as encryption and multi-factor authentication, are crucial to safeguard customer data and prevent fraud.

- Awareness and Education: However, educating customers about agency banking services is critical for adoption. Similarly, public awareness campaigns can help dispel misconceptions and encourage participation.

Conclusion

Finally, white-label agency banking is reshaping Nigeria’s financial landscape, offering banks a powerful tool to expand their services and deliver personalized banking experiences. With its numerous benefits and potential for financial inclusion, this innovative solution is poised to bridge the gap between traditional banking and digital empowerment. As Nigeria embraces white-label agency banking, more Nigerians will gain access to a wide range of financial services, fostering economic growth and prosperity across the nation.