Digital transformation has revolutionized the banking industry, and agency banking is no exception. This blog post delves into the opportunities and challenges that arise from the digital transformation of agency banking. Therefore, by embracing technological advancements, financial institutions, agents, and customers can unlock new possibilities for convenience, efficiency, and financial inclusion.

Expanding Financial Access through Technology:

Digital transformation in agency banking opens doors to broader financial access. Technology-driven solutions such as mobile banking apps, agent banking platforms, and biometric identification systems allow customers to perform transactions anytime, anywhere. This increased accessibility enables individuals in remote areas and underserved communities to overcome geographical barriers and access essential financial services.

Empowering Agency Banking Agents:

Consequently, digital transformation empowers agency banking agents to serve customers more efficiently. With the aid of digital tools and training, agents can offer a wider range of services, including account opening, cash deposits and withdrawals, fund transfers, and bill payments. The automation of routine tasks enhances agent productivity, reduces errors, and allows them to focus on building customer relationships and providing personalized financial advice.

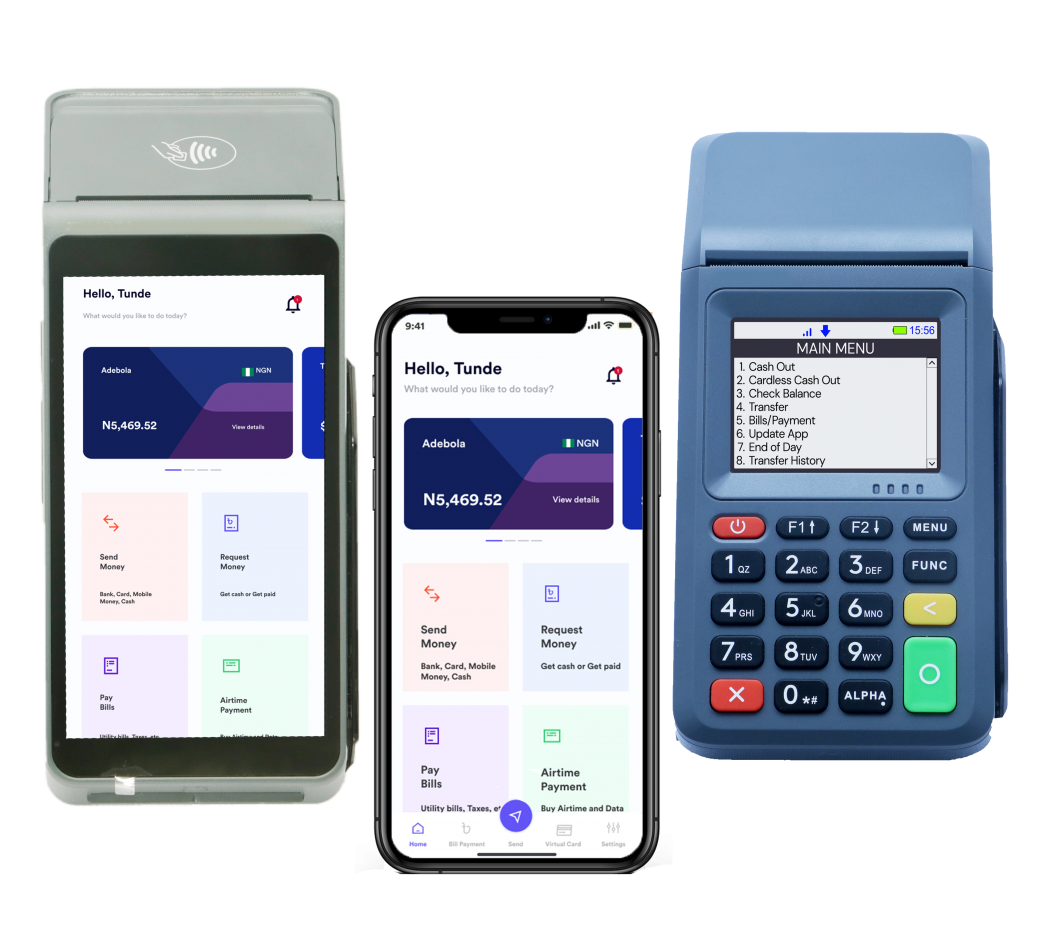

Enhancing Customer Experience and Convenience:

Technology-driven advancements elevate the customer experience in agency banking. Therefore, digital channels provide self-service options, allowing customers to conduct transactions at their convenience. Mobile banking apps and online platforms offer real-time access to account information, transaction history, and personalized financial insights. Furthermore, digital payment solutions enable seamless and secure transactions, reducing the reliance on cash-based transactions.

Strengthening Data Security and Fraud Prevention:

Additionally, digital transformation brings new challenges in terms of data security and fraud prevention. Financial institutions must invest in robust cybersecurity measures to protect sensitive customer information and prevent unauthorized access. Implementing multi-factor authentication, encryption protocols, and real-time fraud detection systems ensures the integrity and confidentiality of customer data, building trust in digital agency banking platforms.

Overcoming Infrastructure and Connectivity Challenges:

Similarly, digital transformation in agency banking heavily relies on robust technological infrastructure and reliable connectivity. Deploying adequate network coverage, expanding internet access, and investing in secure communication channels are crucial for the success of digital agency banking initiatives. Thus, collaboration between financial institutions, technology providers, and telecommunications companies plays a vital role in addressing infrastructure challenges and bridging the digital divide.

Conclusion:

Finally, digital transformation has reshaped agency banking, offering unprecedented opportunities for financial inclusion, convenience, and efficiency. Therefore, by embracing technology, financial institutions, agents, and customers can reap the benefits of a digital ecosystem. However, challenges such as data security, infrastructure limitations, and connectivity gaps must be addressed for sustainable digital agency banking. The future of agency banking lies in striking a balance between embracing innovation and addressing the evolving needs of customers and agents.